A short six months ago, markets were in the midst of a widespread selloff. The dreaded “R” word (recession) began to make the rounds with all fingers pointed at the Federal Reserve – three years into its push for tighter monetary policy (increasing interest rates and unwinding its balance sheet). The 4Q18 selloff took markets down by more than 20%, yet early May has us back to the lofty levels of last fall.

So, what has changed?

- Trade? Ongoing negotiations with tariffs still in place.

- Brexit? Three years later...

- The Fed? Since late December the Fed has turned dovish from hawkish.

As the saying goes, “Don’t fight the Fed” – yet beyond a dovish Fed, has the economic landscape really improved to such an extent? Judging by mainstream headlines of “record highs” and “earnings surprises”, on the surface, it would certainly appear so.

But let’s scratch the surface.

Equity valuations rely heavily on the direction of profit margins – margin expansion a boon to earnings growth and margin contraction a bane. And, over the past several decades, virtually every major driver of profit margin improved.

“Corporations around the world simultaneously benefited from the broad-based decline in labour’s bargaining power, increased globalization, lower anti-trust enforcement, technology allowing for greater scale and lower marginal costs, and lower corporate taxes, interest rates, and tariffs.”

Ray Dalio

These very catalysts have since become hot topics of discussion, which begs the question, is continued margin expansion sustainable?

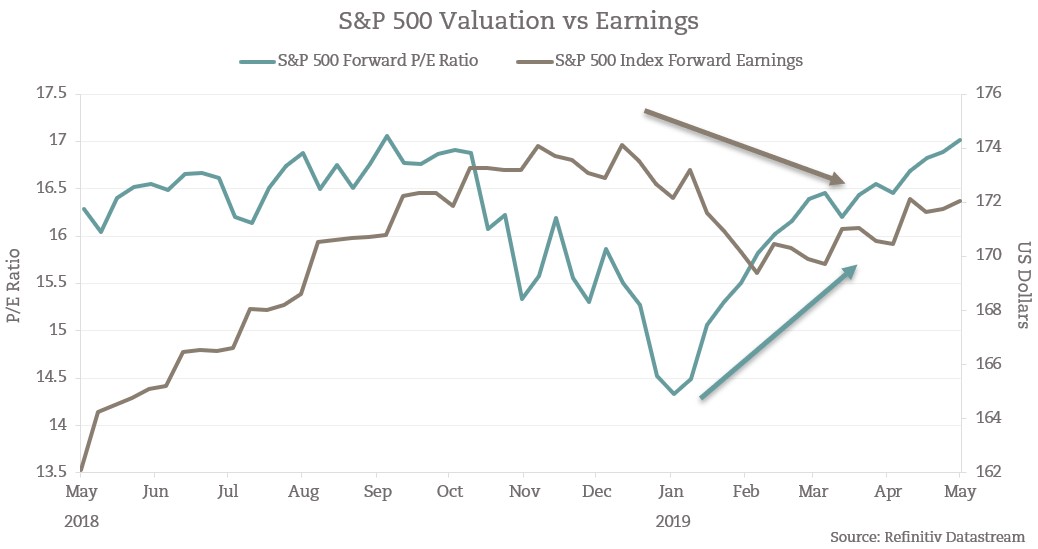

As we navigate through the Q1 earnings season, we see the S&P 500 at new highs, yet it is interesting to note that analysts’ estimates for forward earnings have come down.

In other words, the market rally has not been fueled by earnings growth but rather earnings multiple (P/E) expansion.

Plain and simple, stocks have gotten more expensive. As for the positive headlines, ironically enough, by lowering estimates far enough, an “earnings beat” is all but certain.

Bottom line: Margins are starting to see pressure as many of the historical profit margin drivers are coming under threat; stronger U.S. dollar, higher labour costs, and raw material cost inflation to name a few. Maintaining current levels of profitability will prove challenging and valuations will be fundamental – as always, “It’s what you pay”!